Date: Monday 13 June 2011 Time: 2-3.15pm Venue: LSE campus, venue tbc to ticketholders Speaker: Jean-Claude Trichet Chair: Peter Sutherland

The lecture is in memory of Josiah Charles Stamp, an alumnus and former governor of LSE.

The recent financial crisis has been a turbulent period for policy-makers around the world. Originating in and mostly affecting the financial sector, it has forced central banks to take unprecedented steps to contain the situation and its fallout for the real economy. Overall, this has been achieved, and economic activity is gradually recovering around the world. Risks remain, however, including systemic risks, and the advanced economies are still a long way from achieving sustainable economic growth and job creation.

Jean-Claude Trichet, President of the European Central Bank (ECB), explains how his institution reacted swiftly to the challenges of the financial crisis through non-standard measures. However, at the same time, it has continued to remain faithful to its mandate of maintaining price stability in the euro area over the medium term through standard monetary policy measures. Looking ahead, Mr Trichet also argues that the unwavering actions of the ECB and its decision-making bodies need to be paralleled by a quantum leap in the economic governance of the euro area. The citizens of the euro area want stronger and better coordination of economic and financial policies and are calling for governments to deliver a deeper and more effective economic union.

Born in Lyon, Jean-Claude Trichet is an "Ingénieur civil des Mines", a graduate of the Institut d'études politiques de Paris and holds a Bachelor's degree in economics. He worked in the competitive sector from 1966 to 1968, attended the Ecole nationale d'administration in 1969 and was appointed "Inspecteur adjoint des Finances" in 1971.

He was then assigned to various posts at the Ministry of Finance in the General Inspectorate of Finance and later in the Treasury Department, where in 1976 he became Secretary General of the Interministerial Committee for Improving Industrial Structures (CIASI).

Jean-Claude Trichet was made an adviser to the cabinet of the Minister of Economic Affairs (René Monory) in 1978, and then an adviser to the President of the Republic (Valery Giscard d'Estaing) in the same year. In this capacity, he worked on issues relating to energy, industry, research and microeconomics from 1978 to 1981. He subsequently became Deputy Director of Bilateral Affairs at the Treasury Department from 1981 to 1984, Head of International Affairs at the Treasury and was Chairman of the Paris Club (sovereign debt rescheduling) from 1985 to 1993. In 1986, he directed the Private Office of the Minister of Economic Affairs, Finance and Privatisation (Edouard Balladur), and in 1987 he became Director of the Treasury. In the same year, he was appointed Censor of the General Council of the Banque de France and Alternate Governor of the IMF and the World Bank. He was Chairman of the European Monetary Committee from 1992 until his appointment as Governor of the Banque de France in 1993. He was the Chairman of the Monetary Policy Council of the Banque de France as of 1994, a member of the Council of the European Monetary Institute from 1994 to 1998 and thereafter a member of the Governing Council of the European Central Bank. At the end of his first term as Governor of the Banque de France, he was reappointed for a second term.

Jean-Claude Trichet was elected Chairman of the Group of Ten (G10) Governors on 29 June 2003. He was appointed President of the European Central Bank in October 2003, taking up the position the following month. In 2010 he became Chair of the European Systemic Risk Board.

Suggested hashtag for this event for Twitter users: #lseuro

Ticket Information

This event is free and open to all however a ticket is required. One ticket per person can be requested on Monday 6 June.

LSE students and staff are able to collect one ticket from the New Academic Building SU shop, located on the Kingsway side of the building from 10.00am on Monday 6 June.

Members of the public, LSE staff and alumni can request one ticket via the online ticket request form which will be live on this weblisting after 10.00am on Monday 6 June.

The ticket request form will be online for around an hour from going live. If after an hour we have received more requests than there are tickets available, the line will be closed, and tickets will be allocated on a random basis to those requests received. If after an hour we have received fewer requests than tickets available, the ticket line will stay open until all tickets have been allocated.

One of the key assumptions in the dominant narrative of the Greek crisis is that poverty has exploded to unprecedented levels.Frankly I never expected groundbreaking new levels of poverty because our social welfare system is one of the most inefficient (in terms of poverty alleviated per Euro spent) in the developed world and thus much of the money lost is money that would have been diverted to better-off recipients in the form of either welfare payments of wages. More on this here. But there can't not have been a substantial rise in poverty, and any rise is bad news.

As it happens, a new study is out that models the effects of policy changes on personal incomes from 2009 to 2010. Now if this was a country with a proper policy industry, this study would be cited left, right and centre, and its findings would be spun by all sides in whichever way. But there is no such thing in Greece, so I guess I have to spin by myself.

First things first:

The most common definition of relative poverty (also known as the standard poverty rate) is the % of persons earning less than 60% of the median (not average) income. This is relative in the sense that the poverty line is higher in more affluent societies. For a discussion of absolute poverty in Greece, you may want to take a look here.

By that measure, the study says, 20.1% of Greeks were living under the poverty line in 2009 and 20.9% were doing so in 2010. That’s a very small rise in poverty, in the order of 4%. However, this is not the end of the story. The authors suggest (and I think they are right in doing so) that a better measure of the change in poverty rates would be to benchmark against the 2009 median income, adjusted for inflation. This conveys much better the subjective experience of sliding into poverty – essentially we’re crudely counting the net number of people who have woken up to find themselves unable to afford some pretty basic things that they could afford a year ago.

Benchmarked against this figure, those that are ‘poor by 2009 standards’ made up 25.2% of the population, which means a 25% rise in relative poverty. That’s pretty substantial.The difference in the rate at which poverty levels rose under the two specifications comes from the fact that ALL of Greece saw its income fall in absolute terms in 2010.

So far, so predictable, although it’s important not to trivialise the issue of a 25% rise in poverty. I know some people have made it sound like this figure would be 2000000000%, but the real figure is still horrible news. But there are some findings that really are shocking.

Shocker no 1: Inequality actually fell in 2010, although this was largely because the upper middle class lost ground to the lower middle class (such as it is).

Yup. Although depending on what measure of inequality one chooses, the results can vary a lot. The top quintile of earners (i.e. those earning more than 80% of the population does; though check below for a hint at how well of they are) put even more distance between themselves and the bottom quintile (those earning more than 20% of the population does). But the overall Gini coefficient, the most commonly used measure of income inequality, actually fell. Can the same country become both more and less equal? Of course it can. See how in the graph below:

Shocker no. 2: Public sector cuts reduced inequality

Yup. Why is this? Because 74% of public sector employees belong to the 30% highest-income Greeks. This means the civil service has almost the same share of marginally comfortable staff (realistically this is people earning a net EUR1,200 - 1,300 per month, see below) as the banking sector, the poster-boys of excessive compensation. See below:

Changes to personal income taxation also reduced inequality somewhat, while VAT was hugely regressive and cuts to pensions mildly so.

Now I know there's a grimoire of methodological caveats attached to all of these figures but to me they suggest one thing. It is easy to simplify the facts of the crisis to fit ideological frameworks; only if we dare to look the data in the eye, however, can we evaluate policy. I would add to this the suggestion that raising taxes is very bad for equality, on top of being very bad for growth. The best way, surely, to keep poverty at manageable levels ahead of the inevitable default, is to shift more of the emphasis of our adjustment programme away from tax and onto cutting spending.

TECHNICAL UPDATE:

I know I said there's 'a grimoire of methodological caveats' to the above figures, but following a well-placed question from @side_shore I think I should point out the most important one.

Basically it concerns the accuracy of income reporting. The incomes used in estimating the above figures are of course themselves estimates. There is no database of Greek incomes after all. Basically, the authors have used EUROMOD to extract incomes as stated to the tax authorities. Assuming massive amounts of tax evasion and avoidance, they have adjusted these figures. The assumption is that incomes are under-reported by 1% for salaried employees, 0% for public sector pensioners, 55% for farmers and 25% for the self-employed (see pg. 7 here). These figures are not arbitrary but rather they are taken from this study.

The problem is that, as I mentioned, there is no such thing as a database of personal incomes, nor could there ever be. So what the authors of this last study did was compare incomes reported to the pan-European EU-SILC study with real tax returns in Greece and arrived at the above figures for under-reporting of incomes. The problem, however, is that while people are more honest when responding to survey questions than they are when filing tax returns, that's a far cry from being totally honest. If you make a buzzilion per year, you don't really want to tell somebody over the phone. In fact, if you earn that much you're unlikely to stick around to take the survey. Similarly, if you're very poor you may not want to discuss this over the phone, or you may omit benefits you are receiving from the state either because you don't consider them to be actual income or because you don't know what the particular benefit is called.

The authors of the first study I mentioned do recognise these limitations but argue that the incomes recorded by EU-SILC have been shown to match up to national aggregates. For a full discussion of the extent and sources of under-reporting, see this paper. It tests the data in places like Hungary and Italy, where people can be as crafty as the Greeks sometimes.

Finally, there's a big problem with the tax evasion and avoidance statistics because they reflect 2004 incomes. In 2004, the tax avoidance and evasion landscape didn't look anything like it did in 2010. The authors of the study I discuss here claim that avoidance got worse between 2004-9 and fell in 2010 under pressure from tighter inspection, but there's actually no way of knowing. In fact, it makes sense that the opposite happened as in 2010 incomes got tighter and tax morale (the crucial feeling that one is not an idiot for paying their fair share of tax, a crucial determinant of tax avoidance/evasion) must have fallen as the government's legitimacy fell rapidly. For more on the determinants of tax morale, see my past post here.

What effect these shortcomings would have on the validity of the findings (not the data, mind you) depends on the extent to which people in the top 10% and 30% of earners under-reported their income to EU-SILC. Despite being a European survey, EU-SILC is administered by ELSTAT and, upon being recruited to respond to it, one is informed that refusing to take the survey is punishable by law, much like dodging a Census. Despite assurances that all answers are confidential, this will have put some people's backs up. You can see the precise questionnaire for all past versions of EU-SILC here.

Bear in mind: the top 10% of Greeks are not a very exclusive club. To join them in 2006, you had to have a net income of about EUR36,000 per year (source). Let's call it 40k net in 2010 money. That's a good salary by Greek standards but it's hardly...

To join the top 30%, you needed a net income of about half that, EUR18,000. That's not a princely salary, and in fact I'm not surprised most civil servants get paid more than this; it's just not that much money. This of course also means that most people in the top 10% and 30% brackets are salaried persons who can't really hide their income from the taxman and wouldn't bother to hide from EU-SILC. That said, most of the income of this 10% is concentrated in a few households so if they are massive tax evaders or avoiders then the data is problematic. I don't know how bad the problem is but do look at the validation study I link to above; it should give you a hint.

Very few analyses of the Greek fiscal situation and the inevitable default discuss demographics, which I find frankly baffling. The typical defaulting country is young (see my Greece vs Argentina comparison here). Greece is patently not. Some people think this changes nothing but it changes absolutely everything.

First of all, let's get a few things straight. Demographics can't be talked around. The ageing of Greece's equivalent to the baby boomers is going to happen regardless of whom we vote in to manage it, and regardless of what mandate we give them. (Except perhaps Kill Grandma!). It is a tectonic shift; a force of nature; the wrath of god. As you can see from my friend Diego's comments below, the same forces are at work in Spain; Portugal and Italy aren't far off. In fact, the only exception is Ireland... for now.

Simply put, Greeks are living to a ripe old age, which is fantastic. Long may it continue. But there is a price to pay, and we will pay it in two ways.

The first of these is the complete PWNAGE of the assumptions built into the social security system. Remember, actuarial projections tend to be done on a 50-year basis (see here), so if you get your assumptions wrong, things can get out of hand very quickly. And assumptions were off indeed in the past. In fact, mortality was assumed under EU guidelines to be 33% higher than the ILO would have recommended. This is money that should have been set aside for grandma's old age but was not because she wasn't expected to live to that age. We were literally keeping our fingers crossed, knuckles white, that grandma would die so we wouldn't have to fork out her pension money. Even so, by 2009 the bill for caring for the elderly had reached EUR27.3bn, not counting any health-related spending on older patients. My best guess based on the correlation between the two is that that would be another 2bn per annum. Older Greeks' share of the population is growing in an almost linear fashion [See graph on SeekingAlpha]. Payouts on pensions in Greece (other than private policies) have grown much faster than the Eurozone average (source); this is the third fastest growth rate in Europe, surpassed among others by fellow PIIG Portugal.

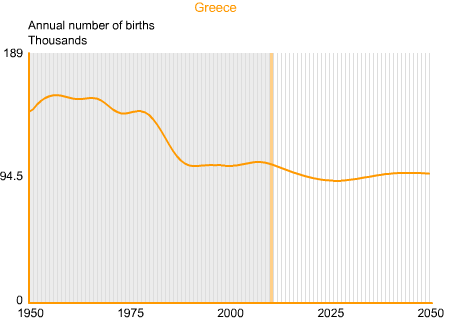

On top of this, fertility in Greece looks like it fell off a cliff going into the 80s (although you may want to look at the very detailed note left below by a helpful contributor and my much more detailed look into the matter here) and never recovered, despite the best efforts of immigrants. There's a number of reasons for this, reviewed here, but essentially, the nation's values and lifestyle had been changing beyond recognition for decades. The 80s only really marked a more decisive turning point. See the trajectory of fertility below (Source UN Statistics Division and INED via Seeking Alpha), although I should note there are alternative forecasts of fertility (H/T @Geo_Gem) which are more optimistic, on the assumption of consistent migration patterns. Which won't happen because of this.

That's part one, but it's not the greater change.

Age changes everything. Older people draw down savings to finance their consumption. They are less likely to chase after jobs. They are less likely to retrain. They work, spend and vote differently. They are much more likely to, let's face it, just die.

Let's start with the spending bit. It's pretty simple to see how age changes consumer behaviour as there are some handy statistics to call upon. Try this table for example. Sure the data are a little dated (2005) but ageing is not a new process so I suspect the key findings will remain the same. At any rate, the graph below shows how much more or less the typical adult equivalent (i.e. either one adult or a minor 'scaled up') consumes in a household where the reference person (typically the head of the household) is 60 or over, versus one where the reference person is 45 to 59. I focus on the latter because they are the main earners and the wealthiest among the Greek population, so how they spend their pennies tends to matter more than how students do.

Let me give you a few hints on what this means. It means the Greek market for drugs and medical treatment will boom. It means the national electricity corp. is worth more than some people think. It means the usual route out of unemployment will soon be as a maintenance/repairman, a cook or a waiter, as opposed to a retail salesperson or clerk. It also means that, long-term, steadily ramping up taxes on alcohol is likely to make more money than taxing tobacco.

You know how the Greek government expects 1bn per annum in VAT from tobacco sales alone? Well the over 60s tend to spend 39% less on tobacco than the 45 to 59ers. When the Greek government tries to sell our Electricity company, they may want to remind prospective buyers that an ageing population is good for them, as the over 60s spend 43% more on fuel than the 45 to 59ers. Of course it will probably spend the increased fuel tax revenue (we expect 7.65bn per annum in various fuel taxes) subsidising shivering grandmas, so better not count on that money. Selling OTE, on the other hand, might be an issue as the over-60s spend 20% less on telecoms than the immediately younger group. The list goes on and on.

If you have been watching Greece over the last couple of days, you will know that Parliament is being peacefully besieged by large numbers of protesters trying their best to emulate the Spanish Indignados. Nor are the protesters in Athens the only ones. Check this map out for a hint at what's happening. Braving the elements, these folks have decided that by telling the Greek Government that they are upset they will somehow make history. I wouldn't be so certain, unless the bar is set abysmally low. Plus I kind of think the Government already knows.

It is perhaps not surprising that the key rallying cry involved in these developments was an internet meme - destined for viral status almost from the start - to the effect that the Spanish Indignados were taunting our complacent compatriots with the chant "Shhh, quiet, we'll wake up the Greeks". Although this was merely a fabrication based loosely on Spanish football taunts, it nonetheless struck a chord. Over Twitter, one user made it abundantly clear to me that in their view the truth of the matter was irrelevant. What mattered was the need to rally the people. This echoes the reactions I got from people forwarding the newly-resurfacedWeisbrot hoax, and makes me wonder whether that whole nasty episode wasn't just a dry-run for this sort of thing. I think we'll be hearing a lot of this sort of noble lie going forward as the great friendly hand of populism reaches for the nation's collective buttocks.

Now to give the protesters their fair dues, the protests appear to me to be genuinely non-factional and peaceful. Union troops from the National Electricity Company were even briefly booed by the assembled crowd. Despite many years of allegations that our murderous anarchist splinter groups (such as these and these) were agents provocateurs planted by governments in order to discredit all legitimate protests, these gatherings have not been disrupted, give or take the odd minor incident.

More to the point, the protestors do not appear to have any recognisable agenda beyond registering a) their numbers and b) their indignation. The only output I've seen so far is a loose collection of rants from the assembled throng charitably christened the minutes of the first assembly (standby for more; there's also been this call for Direct Democracy Now.) At any rate, manifesto items include things like "We have Beauty on our side, against the devious Banker and the evil Politician". In fact the whole thing reads like the kind of thing HR people put on flipcharts while one tries to stay awake during "workshops." Some way to go then, and people will probably have to stop using crayons first.

It amuses me to watch as media commentators visibly try to calculate the chances of this nascent movement ever amounting to anything, and to then watch as half of them slowly -ponderously- align themselves to the protesters, while trying not to be called out as fakers in the process. I wish them well. Me, I'm not too keen on this movement (read on though, I think they can come in handy!) and I won't be even if they take over the entire country.

Question no. 1: Who are they?

Simply put, they are the sum of the non-violent among these guys, these guys and these guys (both latter groups are nonviolent anyway). It's not a naturally cohesive mix; in Spain, maybe this sort of grouping got along well, but in Greece mistrust runs deeper and spirits run higher. It will take a sustained effort to make a movement out of this. I've no way of knowing how many they are, but I would say about 200,000 active so far is a reasonable estimate. Their numbers will grow substantially over the next week, barring any particularly stupid mistakes, as the three groups (non-violent nationalists, defaultniks and disillusioned voters-for-sale) together number much more than this. Frankly, they number in the many hundreds of thousands, so it's only a matter of mobilisation.

Question no. 2: How many are they? I mean really?

I think it's best to be realistic here and consider how many potential supporters this group has. I'd like to give them the benefit of the doubt with regard to this number because these are turbulent times and people tend to jump on bandwagons. Luckily I can run an approximation, using data from the European Values Survey of 2008 (data can be found here). I am only going to assume three things about these people: first, that they would at least consider joining a lawful demonstration. Second, that they believe that Greek society needs to change radically, not by incremental reform. And third, they they had little or no faith in Parliament as of 2008 (I'm allowing the 'little' response as faith in Parliament has slipped substantially since). That's all. I doubt any of the protesters would argue with any of the above. I really believe I'm throwing many more non-Indignados into this calculation than I'm keeping out of it, so I think my estimate is at the very least not conservative. They are, to illustrate, the group highlighted below:

The grand total? 8.4% of the Greek adult population or 625,000 people (calculations here). Where would that put them in parliament, if they were to all turn up and vote for one new party? Just ahead of the Greek Communist Party. They would command roughly 23-24 seats (I'm extrapolating from here).

Question no. 3. How did they use to vote?

According to the model I built above, the Values Survey can give me an answer of sorts to this question, but I must warn you the sample is really tiny, so take it with a massive pinch of salt. The sample is so small that answering this question is like asking a focus group or a room full of people, so don't read these results as statistically robust findings. THEY ARE NOT.

For the most part, these possible Indignados were pretty active voters. Nine out of ten said they would turn up to vote if an election were to be held the following day - which is way better than the average. The breakdown of votes would be as follows:

Now I'm not surprised by these results, although I should caveat them further by saying that the conservative share of the pie is probably under-estimated as the Conservatives were in power in 2008 and thus their voters were more likely to trust Parliament.Similarly the Socialist share of the pie is probably over-estimated, though less so than the conservative slice is overestimated, as many socialist voters will have had a drastic change of heart in the last year.

Question no. 4: What do they want?

It's very hard to hear the triumphalism with which people report on these protests and assume that they are not getting drunk on illusions of power. I believe it is only a matter of time before some charismatic populist stage-dives into this crowd and into mainstream politics. It's going to be almost precisely like this:

Until then, it's important to note that the core of the protesters would probably agree on the following things:

Greece should default on its external debt immediately.

Greece should reverse the fiscal measures taken so far under the Memorandum

Greece should review its constitution in order to ensure further accountability for those in power

Greece should investigate most of the people who have served as Ministers in the last 30 years

Greece should investigate most Greeks with substantial assets abroad

Greece should engage in rapid tax reform aiming to shift a substantial amount of the tax burden to the richest.

Greece should henceforth rely more on plebiscites and less on politicians or technocrats for the purposes of policymaking

Greece should ally itself more explicitly with other peripheral European and developing countries

Question 5: What will they do next?

In short, they will both organise and splinter. As slightly less cohesive and slightly more paranoid versions of the Spanish protests, the Greek ones will organise around issues of security (including the thwarting of agents provocateurs), food delivery, daycare and political speech, in that order. The first three are not contentious, but the latter is, and will become more so the longer the initial wave of protests continues. People will want influence proportionate to what they see as their investment as a matter of the distributive justice that we Greeks are so fond of. The more nights one camps in Syntagma, the more say they will come to expect. Besides, splinter groups of the Greek Left (a major constituent of this moevement) have such a long tradition of choosing fragmentation over effectiveness (more here) and such a deep-seated (and requited) hatred of the nationalists that make up another large segment of the protester population (illustrated perfectly here) that it's only a matter of time before someone mentions policy and the fireworks start.

Question 6: How will they evolve?

I do believe that, as long as they remain civil, these people can be useful as leverage in negotiating better loan terms and a Greek default; Although the Troikans will hardly be crapping themselves at the unrealistic prospect of having a Greek Hugo Chavez across the table from them, this group could swing a closely-fought election.

UPDATE:

One quick way of thinking about the dynamics of the movement is to borrow an analogy from social media monetisation.Social media networks invest in growing their membership at significant cost, against the promise of turning members into paying customers one day. Except not having to pay is critical to sticking with the network. While the service is free, what matters is they way it is delivered, not what the content is. Users make up the content and literally come up with uses for the medium as they go along. All the owners of the network have to do is keep their fingers crossed that eventually the network will become so integral to users' lives that they will be unable to get around paying for it, like a utility. Otherwise, they either hope that they can skim a tiny bit of money out of a very large volume of interactions that inevitably happen through the network, or sell very inobtrusive access to their membership.Either way, investors generally fall for the hype and put massive amounts of resources into the networks regardless of their real prospects.

Now similarly, the Greek Indignados are growing in number. Clearly, they want influence but the more intelligent among them have cleverly made a point of refusing to sign up to a charter of beliefs or policy demands precisely because they realise that this will halt the growth of the movement; which will in turn interfere with the pursuit of power. Sooner or later, they will have to confront this dilemma, although they should have enough committed followers to put off the decision for some time. As they decide, there are three possible dimensions in which the 'movement' can grow (and it can grow in all three simultaneously):

The Movement as Fixture: Campsites become permanent (I'm thinking Parliament Square in London but feel free to insert your own image). Supporters are encouraged to contribute goods, services and their presence when convenient, around a hard core of die-hard campers who are present at almost all times. More importantly, a 'virtual campsite' is set up, with an aggressive social media presence courtesy of sympathetic online and offiline journalists, which provides supporters with an immersive experience of political news and discussion. Just like social media entrepreneurs, protesters probably view this as a preferred scenario.

The Movement as Crowdsourced Think Tank: The movement becomes expert at crowdsourcing political statements via social media or physical assemblies. This produces a steady stream of initially generic political speech, asymptotically converging to the maximum level of seriousness and precision that doesn't constitute an actual political commitment. Crowdsourcing does rely on very careful and skilled moderation, so it will be interesting to see how this will be handled.

The Movement as Recruiting Ground: Essentially this means that relevance is achieved by becoming a recruiting ground for other political agents. As the movement is currently hostile to people with an overt political affiliation, this is a less likely direction of travel and this is unlikely to change. Still, although the Movement cannot allow political parties access to its members in the pursuit of greater relevance, it could do so for other stakeholders that are seen as 'kosher'. Bear with me while I try to visualise this.

Over Easter I went out for shisha with my old friend and reader of this blog, D.V.

D.V. had some kind words for this blog and for myself but noted a flaw in my approach: I was spending a ridiculous amount of time responding, point for point, to every commentator. He noted that this no way to blog on controversial subjects; the time that goes into this sort of thing detracts from useful writing and indeed if I wished to address valid criticism I could do it by simply editing my posts and acknowledging whoever had made the suggestion in the first place. Why not simply go for that?

At the time I agreed that this was the right approach and promised to adopt it. However, I failed to do so for two reasons: first and foremost, because I crave the excitement of comment sparring; it has some addictive quality that I find irresistible. But also because this website is dotted with written commitments to the effect that I will approve and respond to every comment I receive; when I wrote them I actually meant them. All readers, after all, from the most constructive to the downright trolletarian, write comments in order to elicit a reaction of sorts.

Today, however, I was reminded of why he was right. I've just finished another round of comment-sparring from which little that was helpful was learnt on either side but which, in all, took enough of my time to write a whole new post from scratch. Only a small amount of this time was spent getting hold of useful research that I could then use elsewhere in the blog. That can't be right.

And this is, frankly, nothing compared to the troll torrent that followed my #debtocracy and conspiracy theory posts.

As I wrote to the anonymous commentator, I consider it an advantage of this blog that I engage with readers, be they critical or supportive, and I will continue to do this regardless of the time it takes. However, the following things will change going forward:

All comments will be automatically approved without moderation. I will delete only comments that are outrageously offensive to people other than myself, or any comments falsely attributed to other people. As you'll have seen, I have never failed to approve any comments; I've only ever deleted two or three, and all of these were my own.

I will no longer receive notifications of your comments; hence I may ignore some of them, especially if they are attached to older posts. I will strive to read all of them but can't promise this. I apologise in advance.

Ping me on Twitter (@lolgreece) if you want to remind me.

I will not respond to comments with other comments. I will only acknowledge (by editing the main body of posts) comments that are critical of my writing and, of those, only the ones that I find constructive. I will not acknowledge anonymous posts in this way, although if you pick a spurious nickname I'll happily call you that.

All pages on which comments are currently closed will have comments reopened in two months' time from now.

A couple of days ago, a research paper landed in my inbox, authored by small business research celeb Roy Thurik and Phillip Koelinger of Erasmus Univ. in Rotterdam. It's due to appear at the Review of Economics and Statistics sometime next year. Although they are kind enough to acknowledge me as a reviewer my only contribution to this paper was to point out this other fascinating paper to them, which in the end they didn't have much use for : )

What the Thurik and Koellinger paper does is explore the relationship between a) entrepreneurship (measured in multiple ways, including business ownership but also self-reported entrepreneurial activity) and b) the business cycle and provide some explanations for the way in which they are correlated. Data refer to 22 OECD countries from 1972 to 2007. It's a very complex chicken-and-egg story but they find that entrepreneurship is a strong leading indicator of the business cycle at the global level, and a weaker on at the national level. The authors believe this is because at the global level the political cycle gets smoothed out, but that's another day's lecture.

For now I think it's important to point out one country in which the relationship between GDP growth and enterprise is nearly statistically zero. Can you guess which one it is?

You guessed right. The numbers here denote statistical significance, they are almost like the probability (ranging from 0 to 1) that the two variables are unrelated. Thus Greece's 0.99 score means the two variables are almost certainly uncorrelated. I.e. a rise in business ownership in Greece appears to be neither the cause nor the effect of cyclical GDP growth.

Now I must confess that this is the result of only one test, which looks at the relationship between enterprise and real GDP from year to year. Other tests that look at longer-term cycles also returned insignificant relationships for Greece. A test that controls for all but the strongest annual shocks to GDP finds the following:

Any ideas on why enterprise in Greece (and many other OECD countries) doesn't seem to respond to the business cycle, let alone lead it? Probably because a lot of it is not actually enterprise. Not in the sense of taking on uninsurable risks and turning a profit. Remember, enterprise is not a Good Thing in Greece as it is nearly everywhere else in the world (see here and here).

What we have plenty of is Tenderpreneurs - people who will set up 'businesses' for the express purpose of winning government tenders; Zentrepreneurs - people who have no product as such or who have set up 'businesses' when in fact they are empoyees; and Nepotrepreneurs, people who are slowly burning their family's money while pretending to run a business.

More thoughts on this to follow. Possibly soon, possibly not.

Here's a little snippet while I wait for Blogger to get its act together and restore my posts. Readers will note that a pretty devastating failure across Blogger has meant that some of my posts have reverted to past editions of themselves and you will not have been able to post comments for a while.

I'm not sure what the deal is but you can follow the repair work (which Blogger claims is almost complete) here.

Anyway today's FAIL comes from ELSTAT which has published its provisional GDP growth estimates for Q1 2011.

Now although this comparison is a bit stupid, it does raise the question of just how fast Greece is growing. You see, the 0.8% figure is seasonally adjusted real growth. Seasonally adjusted nominal growth is 0.1%. Unadjusted nominal growth is -8.6% and unadjusted real growth is -9.6%. These figures may sound horrible but do bear in mind the Greek economy is highly seasonal, growing in boob-shaped fits and starts, and the adjustments are usually done for a reason.

What does strike me as odd is the cheerful reaction of the FinMin, who basically said that this demonstrates that the revenue shortfall of Q4 2010 was a blip and has not derailed our adjustment plans. R-ight. Apart from the fact that the nominal output of the Greek economy is currently lower now than this time of the year six years ago. And we're still paying our debt in nominal Euros.

In this case though I'm beginning to have my doubts and I need help from any reader who knows how the seasonal adjustment is actually performed by ELSTAT. I know how simple models work but this one is different. To me it looks like there has been a big allowance for seasonal effects in deflating the Q1 2011 GDP figures. I'm not sure why adjusted and unadjusted year on year growth should differ so much, surely yoy captures the seasonal effect in both cases? But I am straying outside my usual prowling grounds here.

Here are the figures, see what you can do:

UPDATE: Fellow statpornographer Greg Farmakis has been in touch to point out that this may be explained by ELSTAT's massive seasonally adjusted GDP series break - the reason why they no longer publish anything but flash figures on this series. Hence also the shocking -6.6% figure for 2010.

Seems to me that if the adjustment isn't good enough for the proper figures, it's not good enough for flash and should not be reported on triumphantly.

Over Easter I went out for shisha with my old friend and reader of this blog, D.V.

D.V. had some kind words for this blog and for myself but noted a flaw in my approach: I was spending a ridiculous amount of time responding, point for point, to every commentator. He noted that this no way to blog on controversial subjects; the time that goes into this sort of thing detracts from useful writing and indeed if I wished to address valid criticism I could do it by simply editing my posts and acknowledging whoever had made the suggestion in the first place. Why not simply go for that?

At the time I agreed that this was the right approach and promised to adopt it. However, I failed to do so for two reasons: first and foremost, because I crave the excitement of comment sparring; it has some addictive quality that I find irresistible. But also because this website is dotted with written commitments to the effect that I will approve and respond to every comment I receive; when I wrote them I actually meant them. All readers, after all, from the most constructive to the downright trolletarian, write comments in order to elicit a reaction of sorts.

Today, however, I was reminded of why he was right. I've just finished another round of comment-sparring from which little that was helpful was learnt on either side but which, in all, took enough of my time to write a whole new post from scratch. Only a small amount of this time was spent getting hold of useful research that I could then use elsewhere in the blog. That can't be right.

And this is, frankly, nothing compared to the troll torrent that followed my #debtocracy and conspiracy theory posts.

As I wrote to the anonymous commentator, I consider it an advantage of this blog that I engage with readers, be they critical or supportive, and I will continue to do this regardless of the time it takes. However, the following things will change going forward:

All comments will be automatically approved without moderation. I will delete only comments that are outrageously offensive to people other than myself, or any comments falsely attributed to other people. As you'll have seen, I have never failed to approve any comments; I've only ever deleted two or three, and all of these were my own.

I will no longer receive notifications of your comments; hence I may ignore some of them, especially if they are attached to older posts. I will strive to read all of them but can't promise this. I apologise in advance.

Ping me on Twitter (@lolgreece) if you want to remind me.

I will not respond to comments with other comments. I will only acknowledge (by editing the main body of posts) comments that are critical of my writing and, of those, only the ones that I find constructive. I will not acknowledge anonymous posts in this way, although if you pick a spurious nickname I'll happily call you that.

All pages on which comments are currently closed will have comments reopened in two months' time from now.

I've often wondered what the quickest way is of showing people how big the stakes are for Greece; how far we could fall.

So I've come up with a little test. It is based on a very basic understanding of growth theory and is a deliberately simplified model. The assumptions behind it are a) that the basic determinant of steady-state per capita income is the stock of capital (physical, human and social) per employee b) capital is mobile (financial more than human, more than physical, more than social) and will flow from countries less well-placed to embed it into production to ones better placed to do so (some evidence here).

Ergo, a broad-based measure of 'competitiveness' should correlate broadly with per capita income, after adjusting for purchasing power parity. And what do you know, it kind of does, as shown below (source here; similar findings here and here).

So here is the test:

1. Take the WEF Global Competitiveness Report for 2011 or any other broad-based comprehensive ranking of economies that you think is a good proxy for their overall ability to put capital to good use. See below for suggestions.

2. Take a sample of countries with a competitive ranking similar to that of Greece, say the five countries immediately above and below us on this ranking. The reason for benchmarking in this way is that the relationship between 'competitiveness' and GDP per capita, if such a thing exists, will be a very noisy one - anything, from oil bonanzas to debt binges, can disrupt it. You could run a regression analysis to smooth that stuff out of the way, and one of my commentators suggests a lot of other treatments below.

3. Look up their per capita GDP in PPP terms, a measurement of average output adjusted for the cost of living in each country. One reader has pointed out that in measuring export competitiveness the PPP conversion is not necessary; if you agree, you may want to use per capita GDP in 2010 dollars instead.

4. Work out the average of these income figures, including Greece.

5. Assume Greek GDP per capita in PPP terms will eventually revert to the mean unless our competitiveness ranking changes. Specify a time period over which the adjustment will take place. If you can't be bothered to, assume the adjustment is asymptotic (i.e. takes forever). The math gets more complicated but hey.

Work this one out and you get the following table:

GC Rank

Country

GDP per capita @ PPP dollars

78

Guatemala

4,885

79

FYR Macedonia

9,728

80

Rwanda

1,217

81

Egypt

6,354

82

El Salvador

7,430

83

Greece

28,434

84

Trinidad & Tobago

21,239

85

Philippines

3,737

86

Algeria

6,950

87

Argentina

15,854

88

Albania

7,453

Average ex GR

8,485

Average

10,298

This means that, in real terms, Greek per capita GDP may be inflated by about 64% and would have to fall by this much to balance out our competitiveness rating. This ratio persists if you take the 2009 WEF data instead, even though the comparator countries are different. If you use the dollar version of this calculation you will get a 74% drop in per capita output.

Given that Greece is unlikely to experience a surge in either fertility or inward migration, all of this fall in per capita GDP will come from internal devaluation. Happily this won't happen overnight but even if it happens over 50 years it will be a serious drag on growth: some -2% annually compared to the baseline of potential growth (whatever that means).

Another way of looking at this is that it took two percentage points of artificially-generated growth per annum to keep Greece from collapsing under the weight of our own uncompetitiveness. Or that the last time GR GDP was at 36% of the current figures was in the late 1960s (triangulated from here and here).

An even better way of looking at this is to consider the graphic again:

This suggests that we can try for a linear combination of two paths: try to become as competitive as Canada or Norway, or devalue to income levels below those of Latvia. For reference, 15% of the Latvian population live in homes with no shower, bath or indoor flushing toilet (source). If you go for something in between, you land in the not entirely horrible position of the Czech Republic (where the above percentage was less than half the Greek one, despite the Czechs being poorer on average).

Of course I realise not everything is about external competitiveness as exports only really make up a small part of the Greek economy. That said, the WEF competitiveness ranking measures a number of factors, such as infrastructure, quality of governance and other forms of social capital which are just as relevant to the domestic economy as they are to exports. Also, with free movement of capital a loss of competitiveness can actually mean that the domestic economy shrinks as investment that would have targeted the domestic market is instead channeled abroad.

I also realise that a lot of the WEF data are survey-based and do not necessarily reflect any fundamental reality. I can't argue with this; if you've got a better bechmark please send it to me. Also, if you don't like the Global Competitiveness measures, another ranking that might work for you would be the Human Development Index, which is less likely to expose you to accusations of neoliberalism. You would have to use a weighted version that ignores GDP otherwise the whole thing becomes too self-referential, but the comparison is still possible.

UPDATE: For the latest developments in this story, see here.

Since the idea of the great EUR50bn Greek asset sale first became a matter of national debate in a staged intramarital spat earlier this year, there's been a good deal of speculation on whether it can be done, how it might be done and what might go under the hammer. Depending on one's predisposition for foaming at the mouth, the purported stakes tend to range from the National Electricity Co., to Greek islands or indeed the Parthenon.

The idea itself is not new. In fact, in a curious twist of fate, the senior opposition party (of whom I am a repentant voter) had proposed the Great Asset Sale as early as mid-2010. They even mooted the original 50bn figure. To hear some in the Left speak of 'selling off the People's property' you might think that a majority of Greek are against privatisations. In fact, the most recent poll on this subject (commissioned by a centre-right leaning daily) found that 41% believe they are 'definitely' necessary, while another 33% believe that they are 'probably' necessary. 58% generally believe they are a good thing. The most popular target for privatisation is the Hellenic Railway Organisation group (a listed company), which as one of our few libertarian MPs (and a minister of finance for a mere 2 years) put it back in 1992, once made more losses than the cost of booking every last rail passenger in the country a taxi.

I've promised to look into this matter in the understanding that our Government is hoping to use privatisations to build a war chest of cash that will help Greece default a little earlier. Alternatively a proper price list of public property could facilitate the equity to debt swaps I've called for here. Either way selling state assets could break an important deadlock because, although we can't default without a primary surplus, the longer you draw out a default that everyone knows will happen, the worse off everyone is. And of course everyone's patience is beginning to wear thin.

This will take some time for me to research properly so please come back to this page later if you have time. Here's what I've got to date.

One place to start digging for past privatisation data is the World Bank's privatisation database, which covers the periods from 1988 to 2008. It is focused on developing countries, but let's face it. That's what we are, too. Alternatively, the European Privatisation Barometer is another option. Registration is required to view the data, but it is free.

Examples of such mass privatisation are scarce; indeed most examples come from post-communist states where mass privatisation programmes were carried out almost overnight. (A very interesting review of this experience showing a link to higher mortality rates can be found here. It shows that social capital is a crucial mediating factor mediating the effects of privatisation on mortality, and I think this will be a telling factor in our case as well.)

Of course moving from communism to (hopefully) capitalism is not the same as the Greek experience will be as we have an experience of things like private ownership, corporate governance, protection of minority investors and the trappings of half-way workable markets. But it can still go very very wrong.

Another good place to start is this review which shows that privatisation tends to improve efficiency in publicly owned enterprises and that this more than makes up for loss of jobs where these do occur. I note that the productivity gains aren't necessarily passed on to consumers (the evidence is not there for me to be able to say this). And by the way privatisations mostly tend to cost middle-managers, rather than blue-collar workers, their jobs (evidence reviewed here).

When I saw this today I thought, that's it. I'm all statporned-out so clear my schedule. This would only have been THE most crucial database updated at THE most crucial moment.

Unfortunately the latest edition of EUKLEMS still only goes up to 2007, though it does include every kind of data one could possibly want on every European economy and a few more besides. And it does so for each of the 72 industries identified at the 2-digit level of the 2007 Standard Industry Classification (SIC07).

EUKLEMS focuses on tracking the inputs and outputs of industries and accounting for productivity. If you are geeks, read up on the methodology here. If you are only interested in Greece, download the Greek dataset here and the Eurozone aggregate dataset here.

Unfortunately in the case of Greece a lack of appropriate data on the prices of intermediate inputs means that we can't get the full suite of findings. In other countries it is possible to do really impressive things like break down real GDP growth into its constituent parts and account for Total Factor Productivity.

But we will settle for what we can get.

Blast from the past: EUKLEMS reminds me of the stuff I used to write for my old masters the FSSC when I was a carefree wee lad. It was, ironically, co-launched with a trade union. What times.

{kind=link}

{kind=link}

{kind=link}

{kind=link}